Here’s the reason I’m not convinced the government can’t afford everyone’s pension

You know the Tory government is saying it has to raise the pension age – for everyone – to 67 because it can’t afford to pay everybody under the original conditions?

I have a doubt about that.

You see, the current basic pension rate is around £130 per week (although the maximum is £168.60)

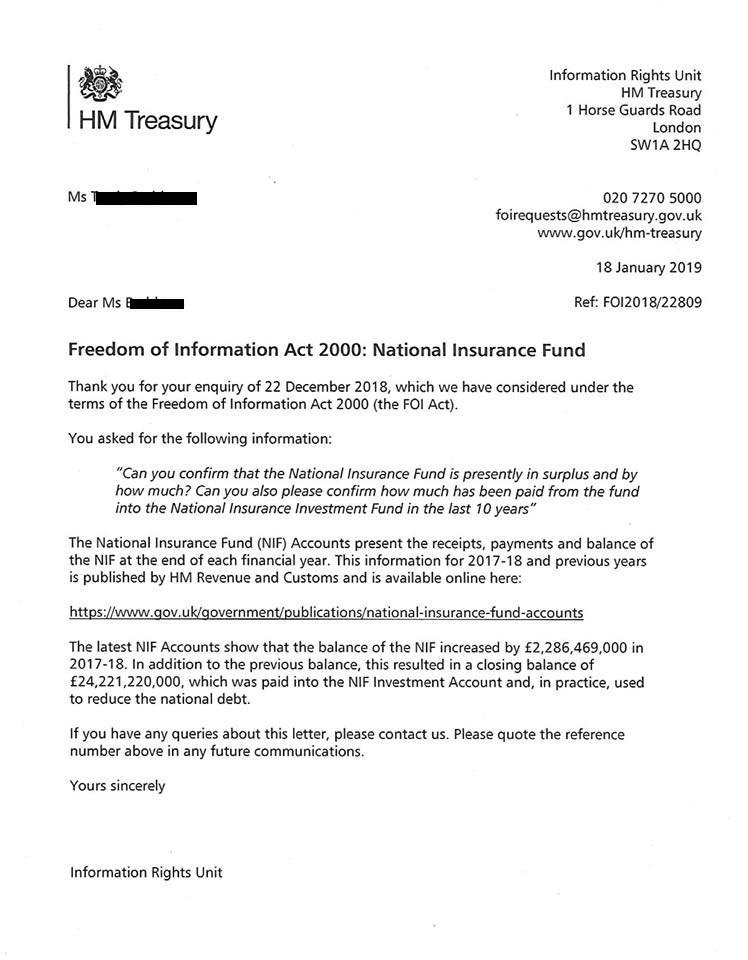

And in January this year, the National Insurance Fund that is supposed to pay for it was in surplus by £24,221,220,000 (see the image above).

Admittedly, considering the number of pensioners in the UK (12 million), it would take only 16 weeks to spend that enormous amount.

But it’s being topped up constantly, it makes money from investments – and the pension-age population is falling because of Tory policies.

That’s why this fund is increasing steadily; on March 31 it stood at £29.5 billion.

And, of course, it would increase much more rapidly if working people were paid properly for the work they do.

Do you get the feeling someone is lying to you?

AFTERWORD: This article has provoked a considerable amount of criticism on Twitter, from some people who claimed to be pensions experts but turned out to be nothing of the sort, and from a few who actually turned out to have something to say.

It is a complicated issue, of course.

But nothing I’ve read has shown the problems are insurmountable by any method other than cutting back the number of people eligible to receive pensions – especially in a nation where wages are being depressed below subsistence levels for working people, while the super-rich are enjoying huge tax breaks (and Boris Johnson is said to want to extend that to cuts in their NI liability too). There are other possibilities, also.

My ultimate feeling, after smiling through the insults and ignorance of many (and the attempts to inform of a few) is still that someone is lying – about the facts of the situation and about what can be done.

I’d like a few opinions from people who don’t claim to be experts on this topic. Do you think that the authorities have been honest about this?

Have YOU donated to my crowdfunding appeal, raising funds to fight false libel claims by TV celebrities who should know better? These court cases cost a lot of money so every penny will help ensure that wealth doesn’t beat justice.

Vox Political needs your help!

If you want to support this site

(but don’t want to give your money to advertisers)

you can make a one-off donation here:

Here are four ways to be sure you’re among the first to know what’s going on.

1) Register with us by clicking on ‘Subscribe’ (in the left margin). You can then receive notifications of every new article that is posted here.

2) Follow VP on Twitter @VoxPolitical

3) Like the Facebook page at https://www.facebook.com/VoxPolitical/

Join the Vox Political Facebook page.

4) You could even make Vox Political your homepage at http://voxpoliticalonline.com

And do share with your family and friends – so they don’t miss out!

If you have appreciated this article, don’t forget to share it using the buttons at the bottom of this page. Politics is about everybody – so let’s try to get everybody involved!

Buy Vox Political books so we can continue

fighting for the facts.

The Livingstone Presumption is now available

in either print or eBook format here:

Health Warning: Government! is now available

in either print or eBook format here:

The first collection, Strong Words and Hard Times,

is still available in either print or eBook format here:

- ☕ Support Vox Political on Ko-fi or donate via PayPal

- 📘 Buy our books — political analysis and satire you won’t find elsewhere

- 📨 Join the mailing list for real headlines, direct to your inbox

- 🔗 Follow us on Facebook and Twitter/X

11 Comments

Leave A Comment

you might also like

- ☕ Support Vox Political on Ko-fi or donate via PayPal

- 📘 Buy our books — political analysis and satire you won’t find elsewhere

- 📨 Join the mailing list for real headlines, direct to your inbox

- 🔗 Follow us on Facebook and Twitter/X

- ☕ Support Vox Political on Ko-fi or donate via PayPal

- 📘 Buy our books — political analysis and satire you won’t find elsewhere

- 📨 Join the mailing list for real headlines, direct to your inbox

- 🔗 Follow us on Facebook and Twitter/X

- ☕ Support Vox Political on Ko-fi or donate via PayPal

- 📘 Buy our books — political analysis and satire you won’t find elsewhere

- 📨 Join the mailing list for real headlines, direct to your inbox

- 🔗 Follow us on Facebook and Twitter/X

I think that you will find that they used the “excess” from the NI fund to go towards paying off the National Debt. Can’t remember where I read this though… The pension is £165 ish under the new rules. So my wife and I will have lost a bit over £60,000

( and 6 years ) by the end of next year when we finally get our pensions :-(

Did they do that between March (when the audited figures I saw were recorded) and now?

I thought the pension amount seemed low but that’s what I got when I looked it up online.

Only one pension per house under Tory law

And IDS thinks 67 is far too soon and we can all work ’til we’re 75, though he didn’t say where all the jobs are, or which employers are queuing up to employ a geriatric workforce. Another slight flaw in his plan is the fact that many people I’ve known have already died in their 50s. In fact, according to the Doctor I’ll be lucky to get past 68, and if I’m very lucky I could make it to 74 at best.

Yup….I made it to 66, never a day off in my life (I’m old – I can lie!) in full health until I had a stroke. Doing fine getting better every day but NOT fit to work. MUst be at least half a dozen friends and colleagues didn’t make it to collect their penson. IDS is an odious man.

Fetching up right behind you at 65, Alan, with unsuccessful chemo cognitive side-effects knocking me out of the labour market in 2007. After my ESA WCA, and PIP appeal (zero to eight points, no better time to appeal – almost 80% success rate!) threatened to kill me throughout last year, I’m now learning to take it easy, not knowing how anyone puts up with current abusive working conditions any more! In many ways I’m glad I don’t have to suffer that abuse, it certainly wasn’t like that when I was last working on a $50ph contract job, on my puter at home in 2005!

Don’t worry, we have that disgraceful liar and torturer IDS’s post code so we’ll get back to him when Uncle Corbyn gets in!

Of course they’ll wants it to give their mates big tax cuts big biz also nay the peasants can go without but wasn’t a question asked in parliament twenty billion gone to pay for the tax cuts hmmm.

That’s not strictly true. The money gets invested to help pay down the national debt – and raised £187 million for this purpose last year – but is still considered part of the National Insurance Fund and may be taken back and used for that purpose whenever necessary.

It seems a lot of nonsense has been said about this, confusing the issue considerably.

Hmm m it was reported in parliament wasn’t it twenty billion or so used but then who am I with my dying brain I wonder but they use benefits monies for their own use no other government in history other than Germany has culled it stock even you have felt this our MPs from day one have had these horror stories told to them but the side rooms of that house with their big talks about it till today talk talk but still it’s rolling on myself I’m ok but my humanity for my fellow man is killing me slowly I not like you a writer of such but life has made me write for my fellow man who brutally treated by this government who should all b tried for their crimes against their own

Since we left the Gold Standard in the 1970’s, banks and the Government have been able to create money by the press of a computer key. Therefore, the Government of the day simply provide guilts as a place where the rich can park their money in safety. It has nothing to do with the Government requiring to borrow money – as they can simply create money as required.

From the above, you can see that the fake news, not being able to afford whatever, is just a way of misleading people, who cannot be bothered or are not interested in economics or how money is created.

I have sent several letters to my MP and various other people regarding the theft of pensions from the 1950’s women onward age groups. There are many protest groups WASPI, Backto60, WPIYPO etc and our group Pension Reformers United which covers all pension injustices.

We are seeking a discussion to try to obtain a fair pension system for everyone as the current one does not do what it was intended to do. i.e. support people in their old age.

Additionally, read David Hencke’s report on the NI pension fund robbery as that explains what happened.

Now, those women born in the 1950’s are struggling without a State Pension after paying in 35 years + National Insurance. Where did that go? Nobody minded equalising pension ages but it would have been helpful if the DWP had mentioned it back in 1995 when the first State Pension increase act was passed.

Many and I mean millions here, not 10 or 20 people, did not know (and some still expect to retire at 60), about the first increase in 1995 until the letter informing them of a further increase came through in 2011. It was very poorly communicated and when they found out it was also very traumatic for them as the State Pension was their only income expected to be due after their 60th Birthday. In some cases only 1 year’s notice that their pension was postponed.

After never having a shot at an occupational pension in their early working life, due to part time working, child bearing, caring duties and additionally occupational pension schemes not including them for various reasons, it was all they had to support themselves at 60 when they retired. That has been removed for in many cases 6 years and above without any safety net for the transitional period.

Many have lost £45K and some never had savings to fall back on so have sold belongings to cover the shortfall. It is very unfair, a theft from people who can’t afford it and it needs to be resolved.

Back to 60 recently had their Judicial Review dismissed and are now appealing that decision.

There was an APPG meeting held last year at which a no cost proposal was put forward which did not in any way compensate for a 5 or 6 year loss of £7,000 a year for 3.8 million women. This appears to be back on the agenda again but will not address this issue and compensate those with the most serious losses.

WASPI are following the Ombudsman route of maladministration which will be put on hold again if there is an appeal by Back to 60.

Meanwhile the DWP are saying they made a concession to the 2011 increase so nobody waited longer than 18 months for that pension increase. They then changed that statement to include the phrase “persuant to the 1995 Act” because they knew that some were actually waiting (in my own personal case) an extra 67 months for their pension. If the APPG proposal goes through this will be their new valueless concession. At no additional cost to be paid from date agreed and with no backpayments. or compensation. A small concession for those at age 63. So those who are almost 66 will get SFA.

A great saving for the magic money tree fund. That’s where 3.8 million women’s contributions who have paid 40 years + National Insurance contributions are sitting.

But we are not going away until this is sorted and we don’t want this in manifestos as a sweetener at a general election, we want it sorted before a General election, so we know who to thank by giving them our vote. Or not as the case might be.

If you want any further information about pensions ask somebody over the age of 50. We didn’t know when we were 50 but by heck we know all about pensions now. This was not done in the name of equality it was done to make savings.

George Osborne actually bragged that “This was one of the least contentious things we did and that it made savings which dwarfed all others”. That was why communication was so poor. It was just a grubby, greedy way of funding vanity projects and bank bailouts by stealing money from the working classes.

Nothing remotely to do with equality which was their excuse, because by doing it this way it made it so unequal as to be unrecognisable. You can’t make something equal by just changing the SPA date. How can it be fair to make it the same for all when there was a different start point? Women were lagging so far behind in the employment and occupational pension game since 1970. We were hobbled from the start and still are. But I repeat “WE ARE NOT GOING AWAY”.

Admin Pension Reformers United.